CFPB Rule 1033: What Financial Institutions Must Know to Stay Compliant

Understand CFPB’s 1033 rule, what it means for financial data access, and how LightBeam helps institutions stay compliant—lawsuit or not.

Bill Schaumann

CFPB Rule 1033, finalized on October 22, 2024, mandates free, secure, API-based access to financial data for consumers and authorized parties, with compliance required by April 2026 (large institutions) and April 2030 (smaller ones).

In October of 2024 the Consumer Financial Protection Bureau finalized its rule that aims to enhance a consumer’s control over their personal financial data. Section 1033 of the Dodd-Frank Act creates new obligations for financial institutions to provide transparency to consumers about their financial data being collected, stored, and processed.

Beginning in April of 2026 in-scope organizations will have to provide consumers with access to their financial data, including transaction history, account balances, and payment initiation information, free of charge and in a usable electronic format. Similar to other privacy regulations, requests from consumers to access their data requires the ability to link stored data to an individual. Understanding the data being processed for an individual requires mature data governance capabilities and accurate interfaces to select the right data for the right consumer.

Requirements

Unlike other regulations like the GDPR or CCPA, 1033 has significantly changed both the time for consumers to receive their information and the methods for organizations to process and store requests.

Traditionally GDPR Data Subject Rights (DSR) requests allowed 30-45 days for processing, and allowed for extensions for data held in off site locations. This cadence allowed for the request to be verified, data analyzed and collected, the creation of a report and any human review to occur.

1033 on the other hand has changed this concept to require a totally automated process capable of receiving and processing requests through a standardized developer API interface within a commercially reasonable time and for the system to maintain a 99.5% uptime.

1033 also requires organizations to;

– Aggregate and normalize consumer financial data (e.g., transaction history, account info)

– Capture and manage explicit consumer consent

– Allow consumers to revoke consent at any time

– Provide machine-readable outputs (e.g., JSON, XML)

– Track and store the requests received and fulfilled for 3 years

– Ability to report on availability, response, and error rates

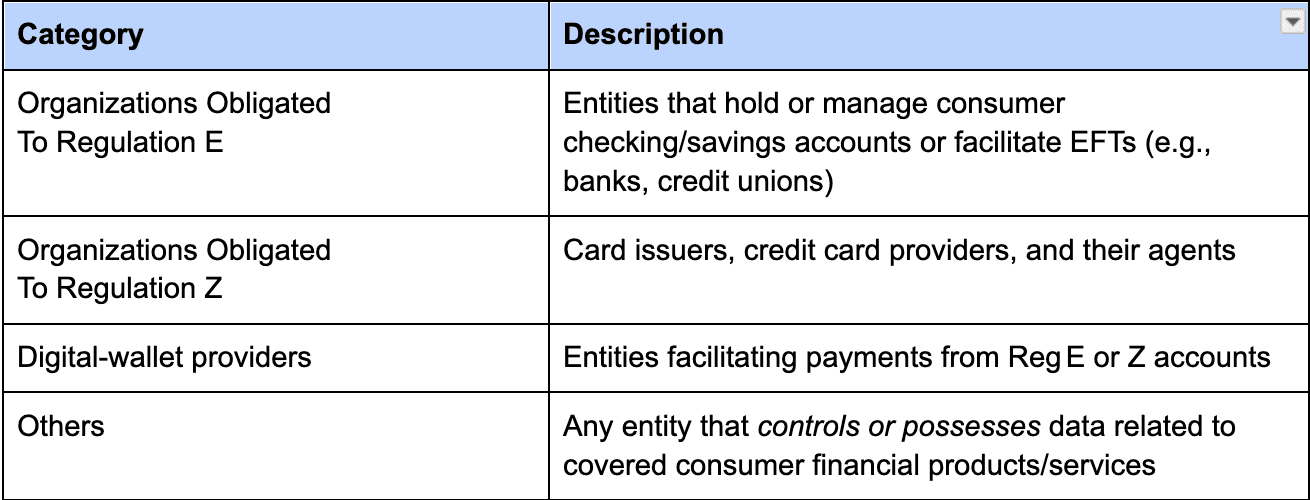

Scope

The 1033 requirements apply to different types of institutions also known as data providers that process financial data.

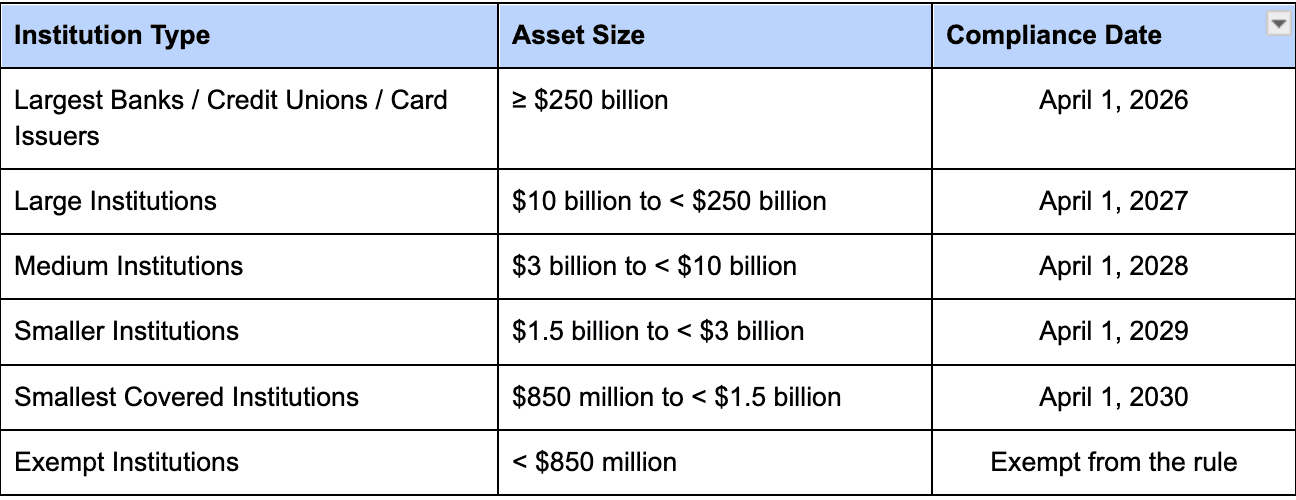

The enforcement time frames are staggered out over several years and are organized by the size of the organization as follows:

Remediation

How LightBeam Helps You Meet 1033 Compliance, without the fire drill. The requirements of 1033 will push the technical capabilities of organizations to fully understand and manage the data they process on consumers. The ability to automatically and accurately identify all data related to an individual consumer and package it for consumption requires organizations to maintain accurate data and process inventories.

Data Subject Rights (DSR) Processing

At LightBeam, we understand the critical importance of efficiently managing and responding to Data Subject Requests (DSRs) while adhering to stringent data protection regulations like GDPR, CPRA, Quebec Law 25, etc. Our DSR Automation Tool, LightBeam PrivacyOps, is here to simplify your DSR processes and ensure compliance with ease.

Identity-Aware Data Discovery

Continuously discover and classify sensitive consumer financial data, transaction history, account balances, and more, across structured and unstructured systems. LightBeam maps every data point back to a real human identity, enabling accurate, per-user data access at API speed.

Consent Tracking

Track consent in real time with our Consent Management Dashboard. We provide all the tools needed to capture and maintain consent status for all individuals in the environment.

Access Governance

Automatically enforce least-privilege access policies, and instantly see who has access to what, and revoke inappropriate access before it becomes a compliance risk.

Real-Time Monitoring and Reporting

LightBeam provides real-time reports in the form of RoPA, PIA, and data inventory reports so you’re always ready for an inquiry or audit.

Conclusion

As of the writing of this blog several lawsuits have been brought challenging the legality of the 1033 rule and it is unclear if it will be enforced in the future. Whatever happens with this rule, LightBeam turns compliance with 1033 and other rules into a scalable, secure-by-default process, so your organization can meet modern expectations for data protection, transparency, and trust.

Reach out to us for more information or a full demo!

FAQ Section

Q1: What is CFPB Rule 1033 and why does it matter?

A1: Finalized by CFPB on October 22, 2024, Rule 1033 implements Section 1033 of the Dodd‑Frank Act, ushering in open banking by requiring financial institutions (data providers) to give consumers—and their authorized third parties—free, secure access to financial data via standardized APIs.

Q2: Who must comply and what are the deadlines?

A2: Larger institutions begin compliance on April 1, 2026; smaller providers have until April 1, 2030. Institutions under $850M in assets are exempt.

Q3: What data is covered under Rule 1033?

A3: “Covered data” includes transactions, balances, upcoming bill info, terms, account details—made available in machine-readable formats.

Q4: What is the current regulatory outlook?

A4: As of July 2025, the CFPB has requested a stay and initiated accelerated rulemaking to substantially revise Rule 1033 in response to legal challenges.